Credit Card Mastery: Free Money or Expensive Trap?

- Neha Sharma

- Apr 8

- 3 min read

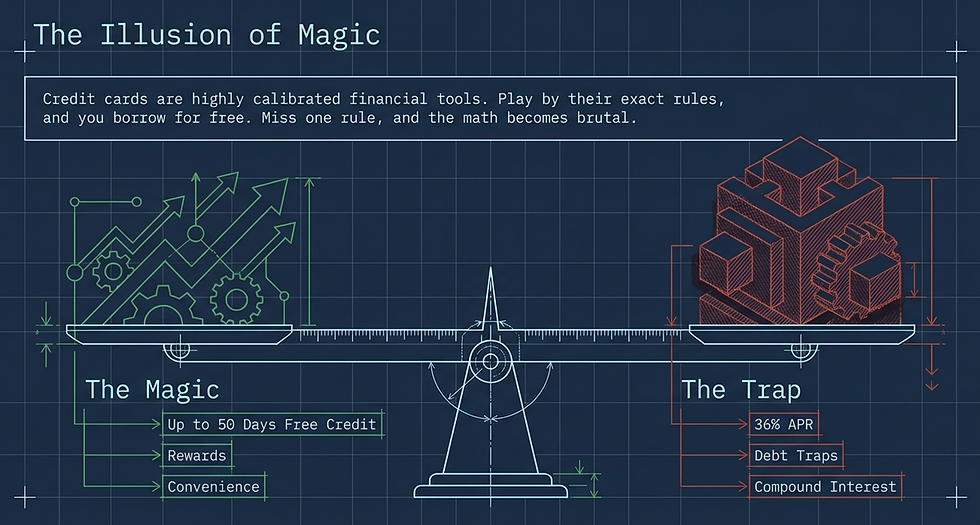

“Get up to 45 days of free credit!” It sounds like magic — buy now, pay later, no interest. But here’s the real trick: the "free" part only works if you play by the bank’s exact rules.

Let’s unpack how credit cards really make money, and how you can use them without ever paying a rupee in interest.

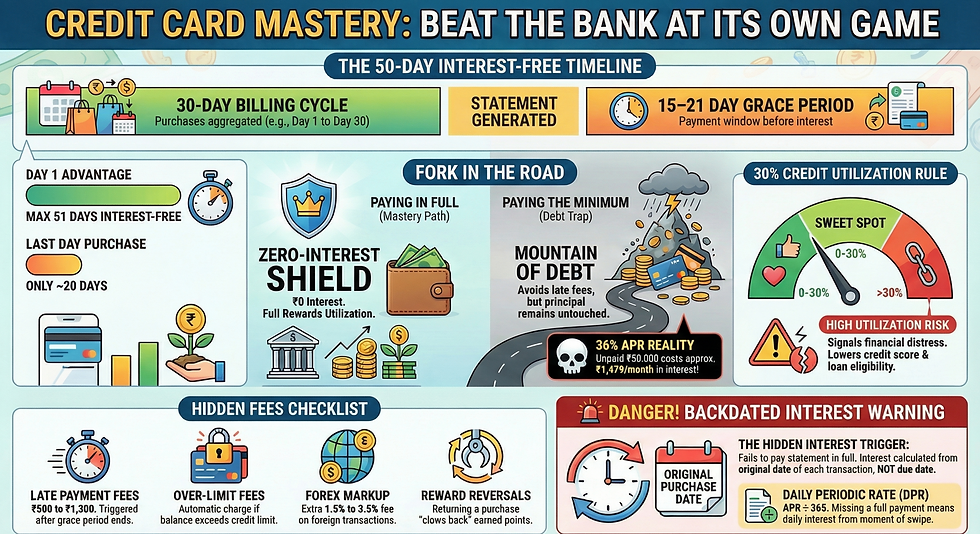

1. The Billing Cycle Magic

Every credit card runs on a billing cycle, usually 30 days long. During this time, you swipe, tap, and spend — and all those transactions pile into one statement.

Once the billing cycle ends, your statement is generated. It lists what you owe and gives you around 15–20 days to clear it.

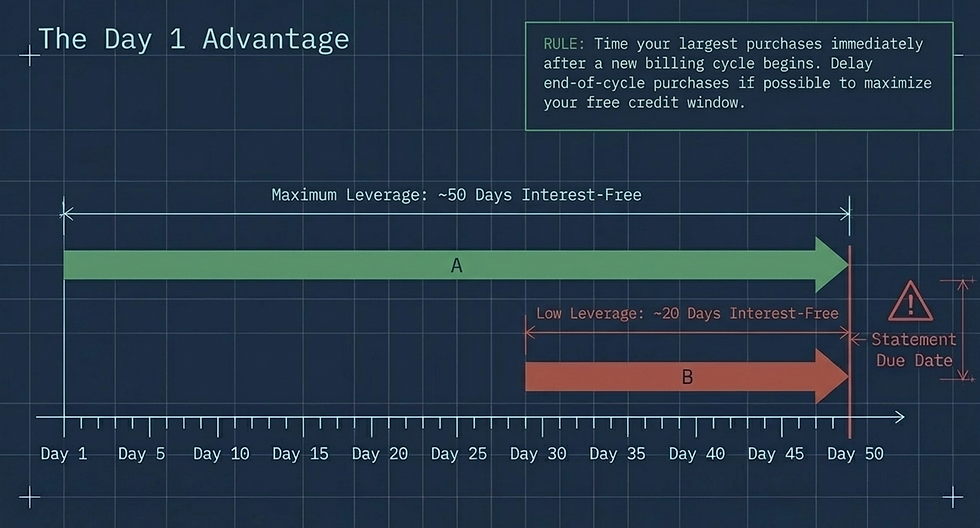

That means your interest-free period can range from roughly 20 to 51 days depending on when you swipe. Spend on day 1 of your cycle, and you get nearly 50 days before payment is due. Spend on the last day, and you get only 20.

Smart move: Time your big purchases right after the new cycle begins — you’ll get the maximum grace period.

2. How Interest Sneaks In (APR Explained)

If you don’t pay in full, banks charge interest using something called the Daily Periodic Rate (DPR).

DPR=APR÷365\text{DPR} = \text{APR} ÷ 365DPR=APR÷365

Daily interest = your outstanding balance × DPR.

Monthly interest ≈ balance × (APR ÷ 12).

Example:If you owe ₹50,000 on a card with a 36% APR, that’s about ₹1,479 in interest every month — just for carrying the balance!

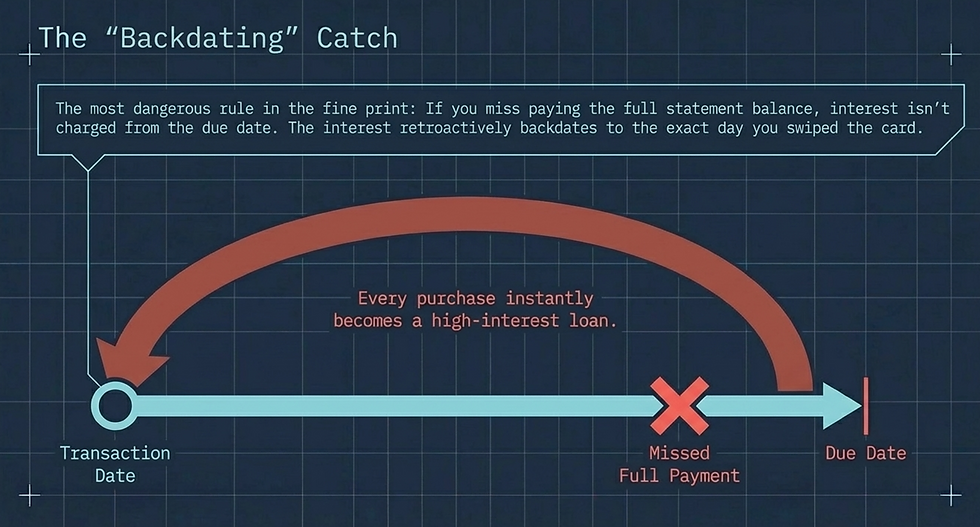

Here’s the catch: interest isn’t charged from your statement date — it’s backdated to the original transaction date.

Miss even one payment in full, and suddenly every earlier purchase starts accruing interest.

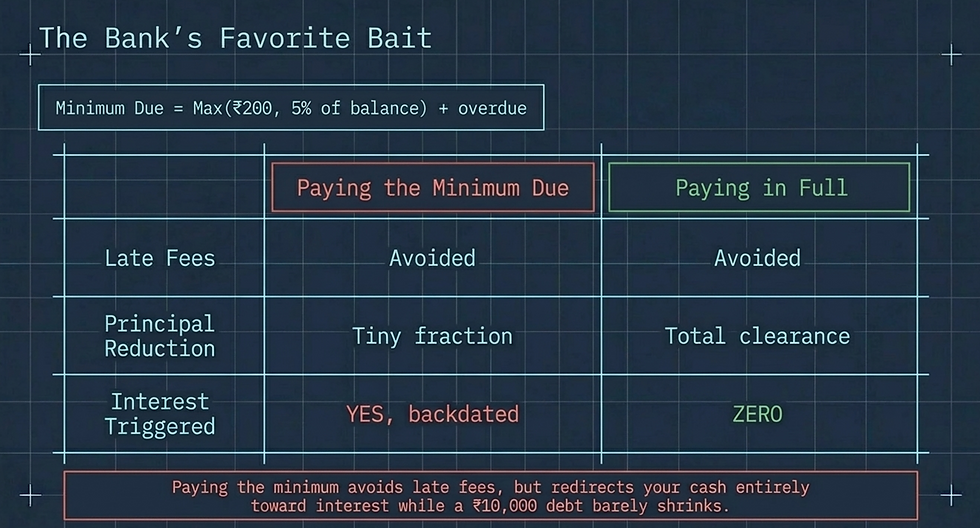

3. The “Minimum Due” Trap

See that tempting “Minimum Amount Due” on your bill? That’s the bank’s favorite bait.

It’s usually:

Min Due=max(₹200,5% of total balance)+any overdue\text{Min Due} = \max(₹200, 5\% \text{ of total balance}) + \text{any overdue}Min Due=max(₹200,5% of total balance)+any overdue

Paying just the minimum avoids late fees — but here’s the trap: most of that payment goes toward interest, not the actual purchase amount. The balance barely shrinks, and you keep paying interest every month.

Over time, a small ₹10,000 debt can turn into a mountain if you only pay the minimum.

4. Mastering the Grace Period

The grace period is your true friend — if you pay your full balance by the due date, you enjoy zero interest every month.

Pro tips:

Shop right after your billing cycle starts to maximize interest-free days.

Never spend near the cycle end if you can delay the purchase.

Always pay the full statement balance, not just the minimum.

Follow these three rules, and you’ll never pay a rupee in finance charges.

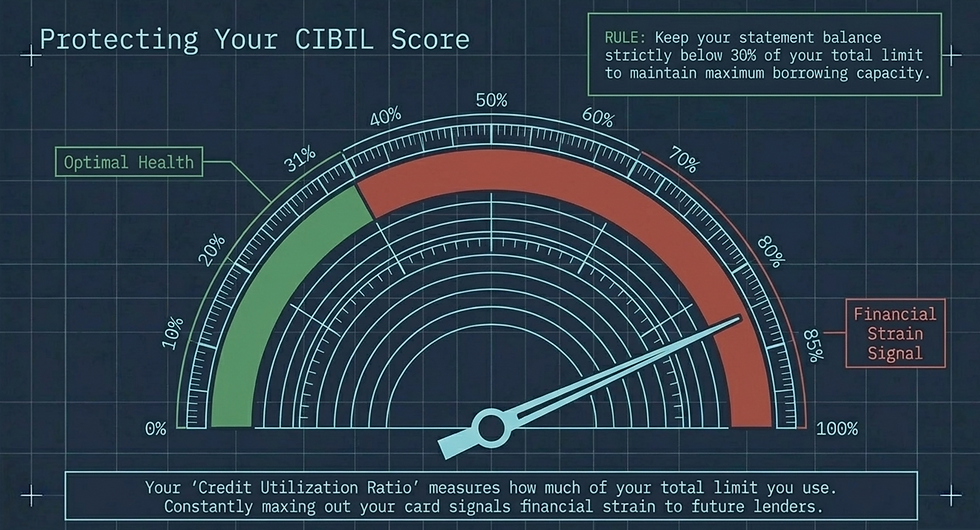

5. Credit Utilization & Your CIBIL Score

CIBIL scores depends on your Credit Card Mastery. Your credit utilization ratio — how much of your credit limit you use — directly affects your CIBIL score.

Keeping usage below 30% shows lenders you’re responsible.

Constantly maxing out your card signals financial strain, which can hurt your borrowing capacity for loans or mortgages later.

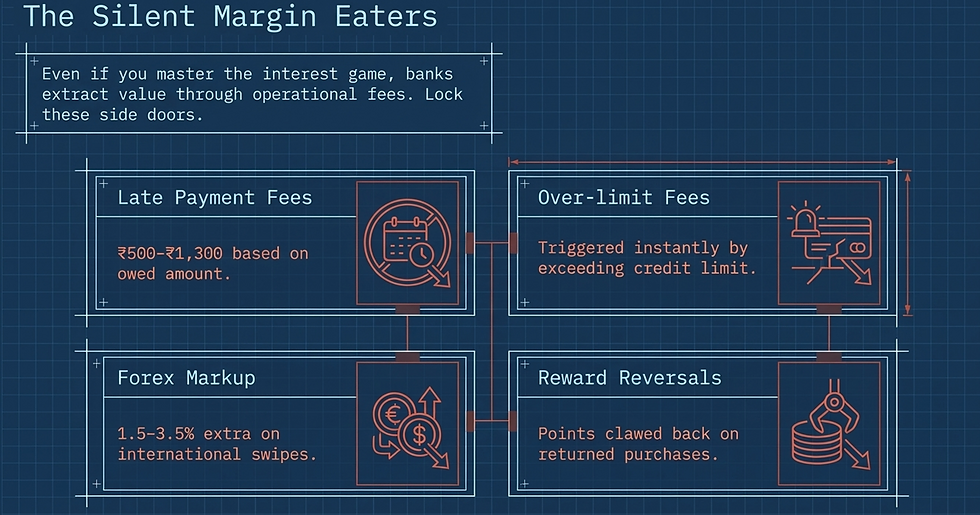

6. Fees That Quietly Eat Your Money

Even if you avoid interest, fees can sneak in through the side door. Watch out for:

Late payment fees: ₹500–₹1,300, depending on how much you owe.

Over-limit fees: Charged if you exceed your credit limit.

Forex markup: 1.5–3.5% extra for international transactions.

Reward reversals: Returned purchases can claw back earned reward points.

Reading the fine print once can save you thousands.

7. The Final Word: Credit Card Mastery needs Discipline

Credit cards aren’t villains — they’re just tools. Used smartly, they offer rewards, convenience, and even free credit for nearly two months.

But forget one rule — paying the full balance every month — and that “free money” quickly turns into costly debt at 36% APR. The math is brutal, and the bank always wins if you slip.

Remember, Mastering Credit Card is easy, Just follow the rule!!

Comments